On October 30, 2020, the Internal Revenue Service (the “IRS”) issued guidance (the “Proposed Rule”) regarding income averaging under Section 42(g)(1)(C) of the Internal Revenue Code of 1986, as amended (the “Code”), for purposes of the low-income housing tax credit (“LIHTC”).

The Proposed Rule addresses designation of low-income units and imputed income limits, provides specifics as to the application of the next available unit rule for income-averaged properties, and creates an opportunity for mitigating actions if a project might otherwise fail to be a qualified low-income housing project.

Comments on the Proposed Rule are due no later than December 29, 2020, and, for best effect, should be submitted electronically through www.regulations.gov (indicate IRS and REG-104591-18).

Income Averaging Set-Aside Test for LIHTC Properties

Code Section 42 provides the foundation for the LIHTC. Under Code Section 42, taxpayers are provided a credit for investments in “qualified low-income buildings.” The amount of the credit is determined by multiplying the “applicable percentage” by the “qualified basis” of the qualified-low income building. In order to be a qualified low-income building, a building must be part of a “qualified low-income housing project” at all times during the compliance period.

Prior to enactment of the Consolidated Appropriations Act of 2018 (Pub. L. 115-141) (the “Consolidated Appropriations Act, 2018”), qualified low-income housing projects were required to meet one of two affordability and occupancy tests: the “20-50 Test,” or the “40-60 Test.”

The Consolidated Appropriations Act, 2018 added income averaging as an additional set-aside option for qualified low-income housing projects, providing a total of three possible set-asides:

-

- The “20-50 Test” in which at least 20 percent of the residential units must be rent-restricted and occupied by tenants whose gross median income is 50 percent or less of the area median gross income (“AMGI”).

- The “40-60 Test” in which at least 40 percent of the residential units must be rent-restricted and occupied by tenants whose gross median income is 60 percent or less of AMGI.

- The “Income Averaging Test” in which at least 40 percent of the residential units must be rent-restricted and occupied by tenants whose income does not exceed a designated “imputed income limitation.” The designated imputed income limitation for any low-income unit must be 20, 30, 40, 50, 60, 70 or 80 percent of AMGI, and the average of the designated imputed income limitations for low-income units within the project must not exceed 60 percent of AMGI.

Designation of Imputed Income Limitations

As described above, in order to satisfy the Income Averaging Test, at least 40 percent of the residential units must be rent-restricted and occupied by tenants whose income does not exceed a designated imputed income limitation for the applicable unit, and the average of the designated imputed income limitations for units within the project must not exceed 60 percent of AMGI. Under Code Section 42(g)(1)(C)(ii)(III), the imputed income limitation for any low-income unit must be 20, 30, 40, 50, 60, 70 or 80 percent of AMGI.

Under the Proposed Rule, the property owner must designate the imputed income limitation for each unit no later than the close of the first year of the credit period. The method of designation is not specifically prescribed by the Proposed Rule, which instead defers to (a) future procedures to be established by the IRS, and (b) procedures established by state or local credit allocation agencies (to the extent those agency procedures are consistent with IRS requirements). An exception to the timing requirement for designation of units is available if a formerly market-rate unit is being converted to a low-income unit, as discussed further below under “Mitigating Actions.”

Next Available Unit Rule

The “Next Available Unit Rule” is intended to address situations in which the income of the tenant of a low-income unit rises above the otherwise applicable income limitation. Under the general Next Available Unit Rule in Code Section 42(g)(2)(D), a unit may continue to be treated as a “low-income unit” for purposes of the LIHTC, even though the occupants’ income has risen to the extent that it exceeds 140 percent of the applicable income limitation, so long as the unit continues to be rent-restricted and the next available unit of equal or smaller size is rented to a new tenant whose income meets the applicable income limitation.

The Consolidated Appropriations Act, 2018 added a new version of the Next Available Unit Rule applicable to properties using the income-averaging set-aside. Under Code Section 42(g)(2)(D)(iii) - (v), a unit does not become “over income” unless the occupants’ income increases above 140 percent of the greater of (a) 60 percent of AMGI; or (b) the imputed income limitation designated for that unit.

In order to use this version of the Next Available Unit Rule, the next available unit of equal or smaller size must still be made available to a qualified low-income tenant. However, the income limitation to be applied to that next available unit will depend upon whether the newly-vacant unit was taken into account as a low-income unit prior to becoming vacant: if the newly-vacant unit was taken into account as a LIHTC low-income unit, that unit’s designated income limitation does not change; if the newly-vacant unit was not a LIHTC low-income unit (i.e., it was a market rate unit), the income limitation applied to that unit must be sufficient to allow the project to maintain an average designated imputed income limitation of 60 percent of AMGI or lower.

The Proposed Rules update existing regulations to be consistent with the income-averaging version of the Next Available Unit Rule established in Code Section 42(g)(2)(D)(iii) - (v), and also addresses situations in which multiple LIHTC low-income units are simultaneously over income.

Under the Proposed Rule, if multiple LIHTC units in a building are over-income (i.e., the income of the tenants’ exceeds 140 percent of the greater of 60 percent of AMGI or imputed income limitation designated for that unit) at the same time, it is not necessary for the owner to comply with the Next Available Unit Rule in a specific order. Renting any available unit of the same size (or smaller) to a qualified tenant maintains the status of all over-income units until the next comparable (or smaller) unit becomes available.

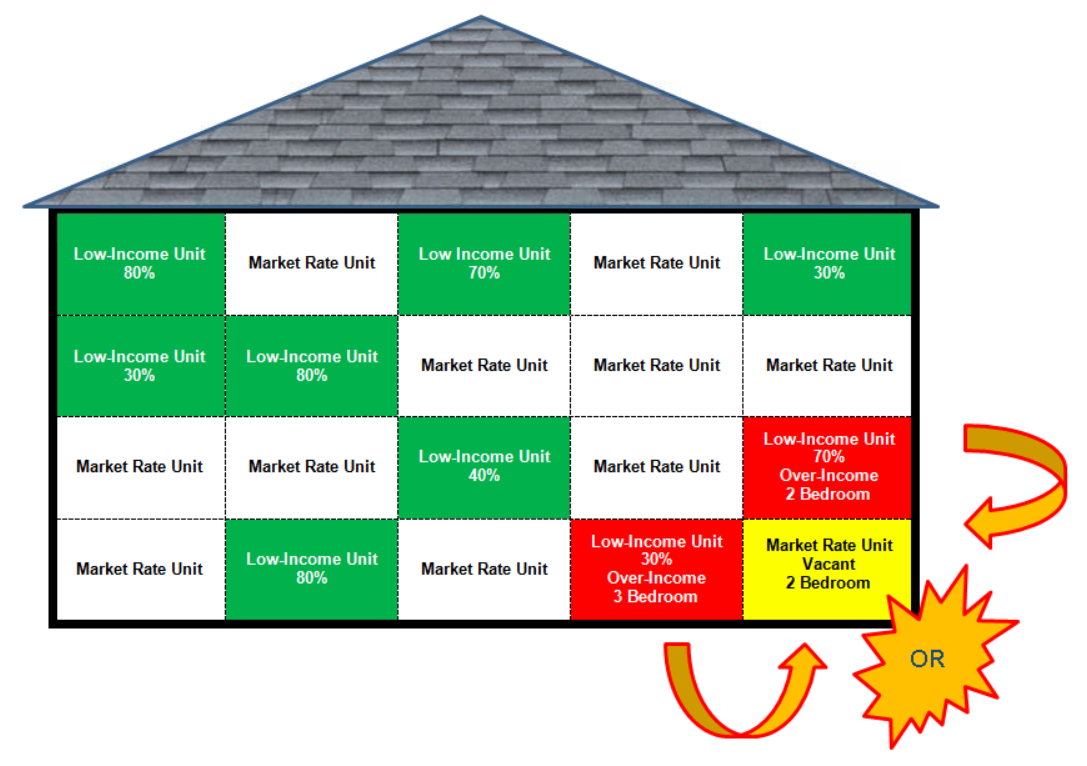

Example: Next Available Unit Rule with Multiple Over-Income Units

To help illustrate the application of the income-averaging version of the Next Available Unit Rule in the context of an income-averaging property, the IRS provided following example:

In a 20-unit LIHTC building, nine units are designated low-income units, including:

-

- Three units at or below 80 percent of AMGI;

- Two units at or below 70 percent of AMGI;

- One unit at or below 40 percent of AMGI; and

- Three units at or below 30 percent of AMGI.

More than 40 percent (45 percent) of the units in this property are designated low-income, and the average of the designated imputed income limitations for low-income units is less than 60 percent (approximately 56.67 percent).

Of these units, two (a 30 percent three-bedroom unit and a 70 percent two-bedroom unit) are over-income. The next available vacant unit is a market rate two-bedroom unit.

Under the Next Available Unit Rule, renting this vacant two-bedroom unit to occupants at either the 30 percent of AMGI level or the 70 percent of AMGI level would allow the property to continue to satisfy both the minimum set aside of 40 percent of units within the property and the maximum average income limitation of 60 percent of AMGI.

Mitigating Actions

The Proposed Rule includes two possible mitigating actions, and the IRS requests comments on a third approach to mitigating actions.

If, at the close of a taxable year, one or more low-income units have ceased to qualify (for instance, because the units have been damaged and are no longer suitable for occupancy under Code Section 42(i)(3)(B)), and this causes the project to fail to satisfy the 60 percent of AMGI maximum for average of imputed income limitations, the owner may take one or more of the following mitigating actions described in the Proposed Rule:

-

- Conversion of a Market Rate Unit – A unit that is not currently a low-income unit may be converted to a market rate unit. The unit must be vacant or already occupied by a tenant who qualifies for residence in a low-income unit at the designated income level (i.e., an owner should not evict tenants in order to access this mitigating action). Designation of converted market rate units must take place on or before the 60th day after the unit is to be treated as a low-income unit.

- Removal of a Low-Income Unit from Averaging – The owner may designate one or more low-income units as “removed units.” A removed unit must meet all the requirements applicable to a low-income LIHTC unit, but will not be taken into account in calculating the average of the imputed limitations of the low-income units. Removal of a unit must not cause fewer than 40 percent of residential units to be designated low-income units. While removal of a unit does not reduce the qualified basis of the building for purposes of recapture, removal of a unit would reduce the project’s qualified basis for purposes of calculating the annual credit amount if the unit is designated as a “removed unit” during the credit period. The owner may terminate a unit’s “removed unit” status at any time.

Alternative Mitigating Action Approach for Comments

In addition to the two mitigating actions described above, the U.S. Treasury Department and the IRS request comments on an alternative mitigating approach. Under this approach, in the event that the average income for a project were to rise above 60 percent of AMGI as of the close of a taxable year due to one or more units ceasing to be treated as low-income units, the owner could redesignate the imputed income level of a low-income unit to return the average to 60 percent of AMGI or below. If such redesignation would cause a low-income unit to be an over-income unit, the Next Available Unit Rule would apply.

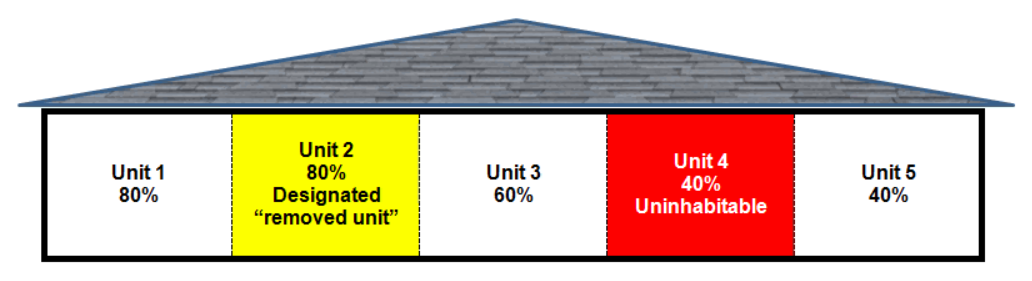

Example: Removal of a Low-Income Unit Mitigating Action

To help illustrate the operation of the removal of a low income unit mitigating action, the IRS provided the following example:

In a five-unit LIHTC building, all units are designated low-income units, with the unit mix shown below. While in Year 1 of the credit period the project is fully leased and occupied, in the second year of the credit period, Unit 4 becomes uninhabitable.

Without Unit 4 included in income averaging, unless mitigating action is taken, the average of the property’s designated income limitations would exceed 60 percent, and the property would fail to be a qualified low-income housing project.

In order to preserve compliance with the 60 percent average AMGI limitation, within 60 days following the close of Year 2, the owner identifies Unit 2 as a removed unit. This allows the project to continue to satisfy the average income test because at least 40 percent of the units are low-income units, and the average of the imputed income limitations of the low-income units does not exceed 60 percent of AMGI.

While Unit 4’s unsuitability for occupancy prevents Unit 4 from being a low-income unit and results in a credit recapture for Year 2, the designation of Unit 2 as a removed unit does not affect the qualified basis for purpose of recapture.

In Year 4, Unit 4 is repaired and the owner also terminates Unit 2’s status as a removed unit. While Unit 4 in uninhabitable, and Unit 2 is a removed unit, neither contributes to qualified basis for purposes of calculating the annual credit amount.

Applicability Dates

The provisions of the Proposed Rule regarding the Next Available Unit Rule are expected to apply to occupancies beginning 60 or more days after the date of publication of the final regulations in the Federal Register. However, the Proposed Rule allows taxpayers to rely on the Proposed Rule with respect to the Next Available Unit Rule for occupancies beginning after October 30, 2020, and before 60 days after publication of the final rule, so long as such Proposed Rule is followed in its entirety.

Other portions of the Proposed Rule are proposed to apply to taxable years beginning after the date of publication of the final rule. However, the Proposed Rule also allows taxpayers to rely on these provisions for taxable years beginning after October 30, 2020, and on or before the date those regulations are published as final, provided that such provisions are followed in their entirety.

Not Addressed in this Summary

While the Proposed Rule does contain specific provisions for deep rent skewed projects described in Code Section 142(d)(4)(B), these nuances are beyond the scope of this summary, as is the specific set-aside contained in 142(d)(6).

In addition, it is always important to remember that LIHTC properties financed with tax-exempt private activity bonds must continue to comply with set-aside requirements under Code Section 142(d), as well as the requirements under Code Section 42, certain of which are addressed in the Proposed Rule. In particular, the concept of income-averaging has not been incorporated into the tax-exempt private activity bond set-aside requirements.

If you have any questions, please contact a member of Foster Garvey’s Senior & Affordable Housing practice.